When Capital Becomes Compute

How equity, infrastructure, and compute are reinforcing each other beneath the AI narrative

NVIDIA is expected to finalize an equity investment of roughly $30 billion into OpenAI as part of a funding round valuing the company near $830 billion. Last September, the relationship carried a much larger headline number (up to $100 billion structured in staged commitments) ~ but that version never progressed beyond a memorandum of understanding. What matters now isn’t the change in size. It’s how the capital is positioned and what it is likely to do next.

A meaningful portion of this funding will circulate directly back into NVIDIA hardware. OpenAI raises capital. OpenAI expands compute capacity. NVIDIA strengthens revenue visibility and deepens its position inside the infrastructure layer. The money doesn’t linger. It converts into GPUs, networking, data center buildouts, and long-duration supply agreements. Equity is functioning as fuel for physical capacity.

This dynamic isn’t isolated. Meta has been securing large volumes of NVIDIA chips for its own AI infrastructure expansion. Western Digital has said its HDD capacity for 2026 is effectively sold out to enterprise and cloud demand. Memory executives have described supply as a constraint as high-bandwidth memory tied to AI accelerators tightens. These developments show infrastructure absorbing demand well ahead of the application layer.

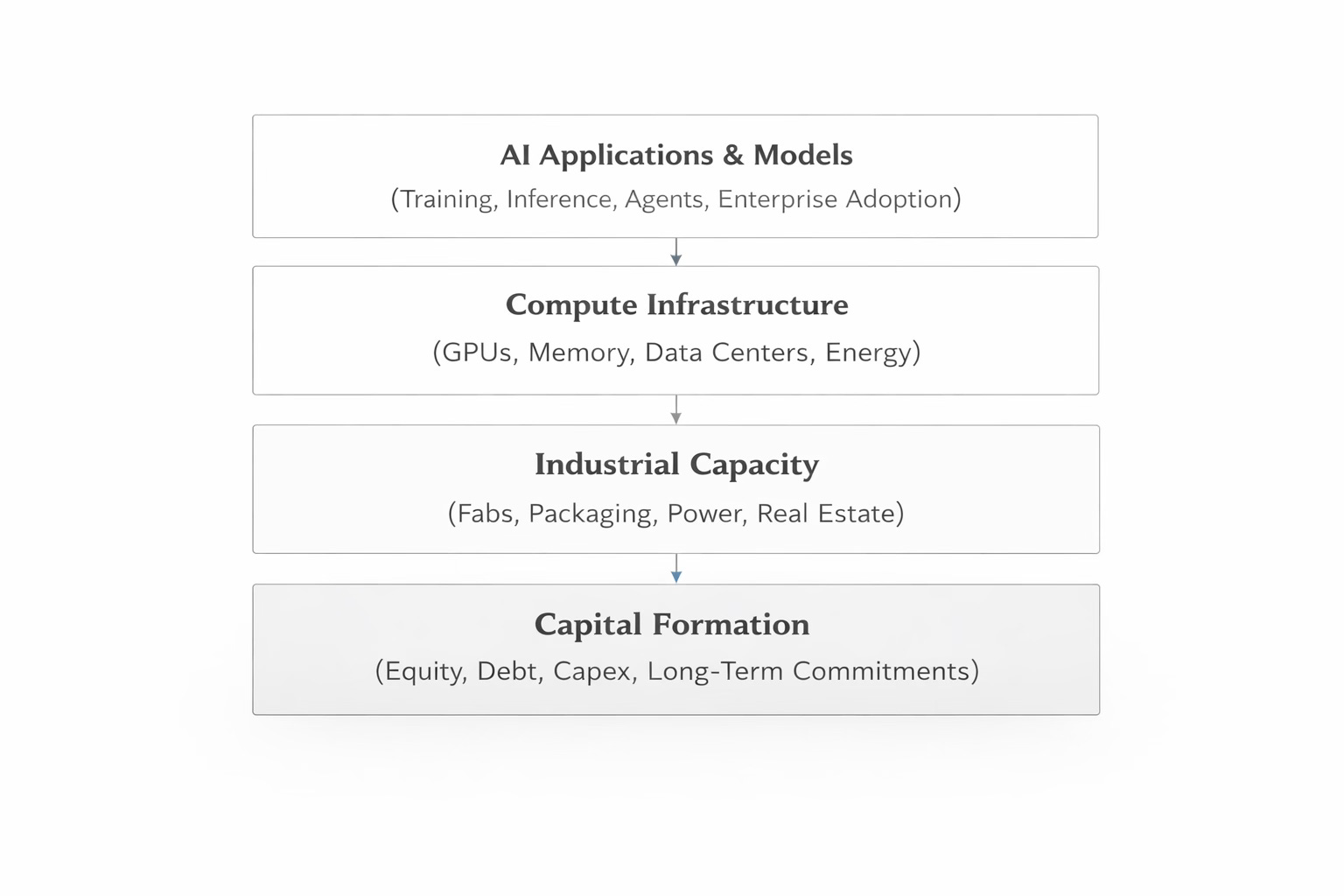

For most of the past year, discussion around artificial intelligence has centered on models ~ which one benchmarks higher, which handles longer context, which writes cleaner code. Those comparisons are useful. The capital being deployed beneath it tells a more durable story. Infrastructure spending continues to expand. Hyperscaler capex has returned to levels that resemble industrial investment cycles more than traditional software scaling. Compute demand absorbs supply as quickly as it comes online.

Compute is not abstract. It depends on fabrication capacity, advanced packaging, energy contracts, cooling systems, and data centers that take years to permit and build. Memory supply cannot expand overnight, and neither can grid infrastructure. As AI workloads move into production, those physical constraints shape economic outcomes.

The NVIDIA - OpenAI structure sits directly inside that reality. When equity funding is closely linked to hardware procurement, it reveals where pressure exists. Training large models is capital intensive. Running inference at scale is capital intensive. Enterprise commitments require throughput and reliability. If capacity were abundant relative to demand, funding would be allocated differently. Instead, capital is being mobilized to secure access.

There is also a capital markets dimension that deserves attention. When infrastructure absorbs large amounts of funding, the distribution of value across the stack adjusts. Suppliers with constrained assets often gain pricing power and visibility. Application-layer businesses, particularly those still refining monetization models, operate within tighter cost boundaries. Markets tend to recognize this before the operating results fully show it. Multiples compress where cost intensity rises and consolidate where supply remains scarce.

For finance and FinOps leaders inside AI-heavy organizations, this is not an abstract observation. Compute exposure increasingly behaves like infrastructure exposure. Long-term commitments, reservation strategies, utilization discipline, and capacity forecasting become strategic levers rather than reporting exercises. Margin models depend on assumptions about access, pricing stability, and workload growth. Small errors in those assumptions compound quickly at scale.

None of this suggests that model innovation slows or that competition disappears. Models will continue to improve. Tools will become more capable. Distribution will matter. Underneath that progress sits a capital base that is large, physical, and time-bound. Data centers cannot be provisioned with a prompt. Memory supply cannot be expanded overnight. Energy contracts cannot be renegotiated in a week.

The funding round matters because of what it aligns. Equity capital and industrial capacity are moving in lockstep. Funding is reinforcing the physical layer of the AI economy in real time.

That alignment changes how risk is distributed. It shifts duration risk across the stack and repositions negotiating power toward suppliers with constrained assets. It also clarifies why cost discipline, capital planning, and infrastructure literacy are becoming executive competencies rather than technical specialties.

The conversation around AI often gravitates toward capability. The underlying reality is about capacity.

And capacity, once financed at scale, reshapes the system around it.